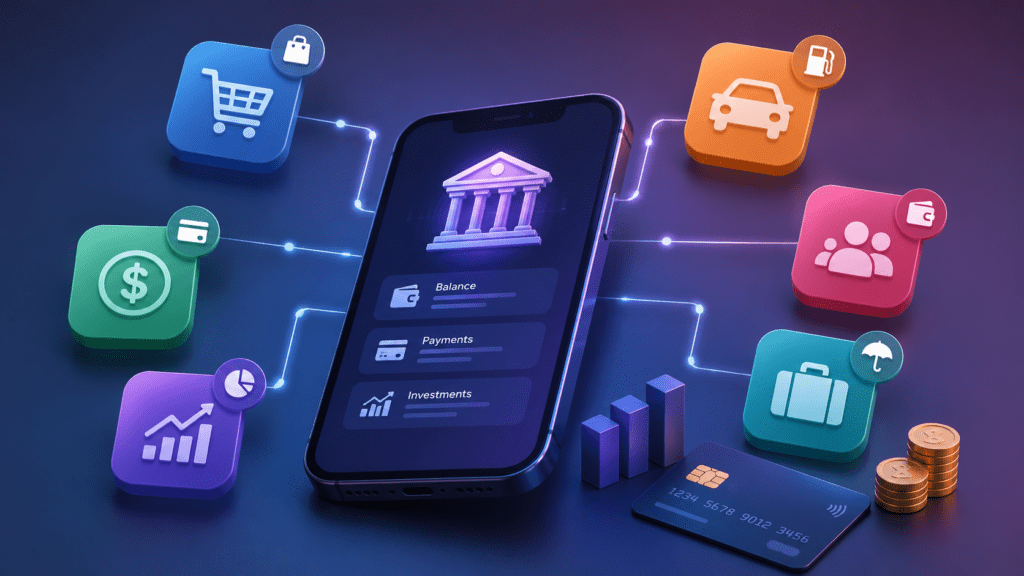

Banking has traditionally required customers to visit a bank branch, log into a dedicated banking platform, or download a financial institution’s app. Today, that model is rapidly changing. Consumers can apply for loans while shopping online, make payments through social media platforms, and access investment tools without ever interacting directly with a traditional bank.

This shift is being driven by the growth of fintech and embedded finance, a trend that allows non-financial companies to integrate banking services directly into their digital experiences. As businesses look for new ways to serve customers, embedded finance is transforming how people access financial products and services while making everyday transactions faster and more convenient.

What Is Embedded Finance?

According to Investopedia’s explanation of embedded finance, the concept refers to integrating financial services into non-financial platforms, allowing users to access banking functions without leaving the apps or websites they already use.

Rather than redirecting customers to a separate bank, retailers, technology companies, ride-sharing platforms, and social media networks can offer payment processing, lending, insurance, and investment services directly within their ecosystems.

A familiar example is the buy now, pay later option offered by many online retailers. Instead of applying for financing through a bank, customers can secure credit instantly during the checkout process. Similar experiences now exist for business loans, digital wallets, and even stock investing.

The technology behind this transformation is largely powered by banking-as-a-service providers and application programming interfaces (APIs), which allow businesses to connect sophisticated financial tools to their existing platforms without becoming regulated banks themselves.

Why Consumers Are Embracing Embedded Finance

One of the biggest drivers behind the growth of embedded finance is convenience. Modern consumers expect seamless digital experiences, and switching between multiple platforms creates friction.

When financial services are integrated directly into an app, users can complete transactions more efficiently. A customer shopping online can access financing without opening another website. A freelancer can receive payments, track income, and manage cash flow through a single platform. Investors can buy shares through apps they already use daily.

Research from McKinsey suggests that embedded finance has the potential to significantly expand access to financial services by meeting customers where they already spend their time online.

This accessibility is particularly important for consumers who may have previously found traditional banking products difficult to access or understand. By simplifying processes and reducing barriers, fintech companies are helping democratise financial services for a broader audience.

How Businesses Benefit From Integrated Financial Services

The rise of embedded finance is not only benefiting consumers. Businesses are discovering that financial products can strengthen customer relationships while creating new revenue opportunities.

Retailers can increase sales by offering financing at checkout. Marketplaces can streamline payments for buyers and sellers. Technology platforms can improve customer retention by becoming a one-stop destination for multiple services.

For many companies, financial products are becoming a natural extension of the customer experience. Rather than serving solely as a provider of goods or content, businesses are evolving into ecosystems that support a wide range of customer needs.

This transformation has accelerated across industries, from e-commerce and transportation to healthcare and social media. Companies that successfully integrate financial tools can create smoother customer journeys while gathering valuable insights into user behaviour and spending patterns.

The Challenges Behind the Convenience

Despite its rapid growth, embedded finance also raises important questions around regulation, security, and consumer protection.

Many consumers may not fully understand which company is providing the underlying financial service when they apply for a loan or open a digital wallet within another app. Transparency becomes increasingly important as financial products become less visible behind the user interface.

Organizations such as the Consumer Financial Protection Bureau continue to emphasize the importance of clear disclosures, responsible lending practices, and data privacy safeguards as financial products become more deeply integrated into everyday digital experiences.

As regulators adapt to the changing landscape, businesses will need to balance innovation with trust. Consumers are more likely to embrace embedded finance when they clearly understand how products work and how their personal data is being used.

The Future of Banking May Be Invisible

The most significant impact of embedded finance may be that banking becomes less noticeable. Rather than seeking out financial services, consumers increasingly encounter them exactly when they need them.

Whether it is securing financing during an online purchase, investing through a mobile app, or receiving instant payments through a marketplace, financial products are becoming woven into the fabric of digital life.

As fintech innovation continues to accelerate, embedded finance is poised to reshape how people interact with money. The companies that succeed will be those that make financial services feel less like separate transactions and more like a natural part of the customer experience.

Industry experts expect the broader embedded finance ecosystem to continue expanding as consumers increasingly favor seamless digital experiences over traditional banking channels.

The future of banking may not involve more banking apps. Instead, it may involve banking capabilities quietly powering the digital experiences consumers already use every day.